Inflation Indexes and Curves 2 (Quantlib comparison)#

This guide replicates and is a comparison to the Quantlib tutorial page at https://www.quantlibguide.com/Inflation%20indexes%20and%20curves.html

Inflation Indexes#

Historical index fixings in rateslib should be indexed to the 1st of the appropriate inflation month.

[1]:

from rateslib import *

from pandas import Series

[2]:

inflation_fixings = [

(dt(2022, 1, 1), 110.70),

(dt(2022, 2, 1), 111.74),

(dt(2022, 3, 1), 114.46),

(dt(2022, 4, 1), 115.11),

(dt(2022, 5, 1), 116.07),

(dt(2022, 6, 1), 117.01),

(dt(2022, 7, 1), 117.14),

(dt(2022, 8, 1), 117.85),

(dt(2022, 9, 1), 119.26),

(dt(2022, 10, 1), 121.03),

(dt(2022, 11, 1), 120.95),

(dt(2022, 12, 1), 120.52),

(dt(2023, 1, 1), 120.27),

(dt(2023, 2, 1), 121.24),

(dt(2023, 3, 1), 122.34),

(dt(2023, 4, 1), 123.12),

(dt(2023, 5, 1), 123.15),

(dt(2023, 6, 1), 123.47),

(dt(2023, 7, 1), 123.36),

(dt(2023, 8, 1), 124.03),

(dt(2023, 9, 1), 124.43),

(dt(2023, 10, 1), 124.54),

(dt(2023, 11, 1), 123.85),

(dt(2023, 12, 1), 124.05),

(dt(2024, 1, 1), 123.60),

(dt(2024, 2, 1), 124.37),

(dt(2024, 3, 1), 125.31),

(dt(2024, 4, 1), 126.05),

]

dates, values = zip(*inflation_fixings)

fixings = Series(values, dates)

Rateslib contains an index_value method that will determine such for a given reference value date and other common parameters.

[3]:

index_value(

index_lag=0,

index_method="monthly",

index_fixings=fixings,

index_date=dt(2024, 3, 15)

)

[3]:

np.float64(125.31)

For example to replicate the Quantlib example of a lagged reference date we can use:

[4]:

index_value(

index_lag=3,

index_method="daily",

index_fixings=fixings,

index_date=dt(2024, 5, 15)

)

[4]:

np.float64(124.79451612903226)

Inflation Curves#

Create a nominal discount curve for cashflows. Calibrated to a 3% continuously compounded rate.

[5]:

nominal_curve = Curve(

nodes={dt(2024, 5, 11): 1.0, dt(2074, 5, 18): 1.0},

interpolation="log_linear",

convention="Act365F",

id="discount"

)

solver1 = Solver(

curves=[nominal_curve],

instruments=[Value(dt(2074, 5, 11), metric="cc_zero_rate", curves="discount")],

s=[3.0],

id="rates",

instrument_labels=["nominal"],

)

SUCCESS: `func_tol` reached after 8 iterations (levenberg_marquardt), `f_val`: 4.2178219398368675e-19, `time`: 0.0071s

Now create an inflation curve, based on the last known CPI print, calibrated with zero coupon inflation swaps rates. Notice that an inflation curve starts as of the last known fixing as its index_base. This is similar to Quantlib, not be design, but by necessity since this is the only information we have that can define the start of the curve.

[6]:

inflation_curve = Curve(

nodes={

dt(2024, 4, 1): 1.0, # <- last known inflation print.

dt(2025, 5, 11): 1.0, # 1y

dt(2026, 5, 11): 1.0, # 2y

dt(2027, 5, 11): 1.0, # 3y

dt(2028, 5, 11): 1.0, # 4y

dt(2029, 5, 11): 1.0, # 5y

dt(2031, 5, 11): 1.0, # 7y

dt(2034, 5, 11): 1.0, # 10y

dt(2036, 5, 11): 1.0, # 12y

dt(2039, 5, 11): 1.0, # 15y

dt(2044, 5, 11): 1.0, # 20y

dt(2049, 5, 11): 1.0, # 25y

dt(2054, 5, 11): 1.0, # 30y

dt(2064, 5, 11): 1.0, # 40y

dt(2074, 5, 11): 1.0, # 50y

},

interpolation="log_linear",

convention="Act365F",

index_base=126.05,

index_lag=0,

id="inflation"

)

solver = Solver(

pre_solvers=[solver1],

curves=[inflation_curve],

instruments=[

ZCIS(dt(2024, 5, 11), "1y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "2y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "3y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "4y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "5y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "7y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "10y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "12y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "15y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "20y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "25y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "30y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "40y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "50y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings=fixings),

],

s=[2.93, 2.95, 2.965, 2.98, 3.0, 3.06, 3.175, 3.243, 3.293, 3.338, 3.348, 3.348, 3.308, 3.228],

instrument_labels=["1y", "2y", "3y", "4y", "5y", "7y", "10y", "12y", "15", "20y", "25y", "30y", "40y", "50y"],

id="zcis",

)

SUCCESS: `func_tol` reached after 8 iterations (levenberg_marquardt), `f_val`: 1.4302416694642844e-17, `time`: 0.0439s

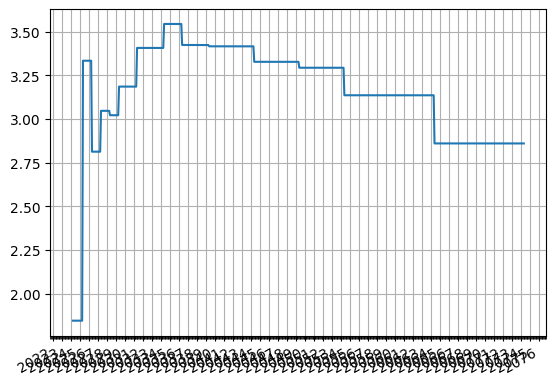

The data can be output to a table or plotted as below.

[7]:

inflation_curve.plot("1m")

[7]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x10e14d950>])

Some of the forecast values from the curve can be obtained directly from Curve methods.

[8]:

inflation_curve.index_value(dt(2027, 4, 1), index_lag=3, interpolation="monthly")

[8]:

<Dual: 135.440324, (inflation0, inflation1, inflation2, ...), [-0.0, -0.0, -50.9, ...]>

[9]:

inflation_curve.index_value(dt(2027, 4, 1), index_lag=0, interpolation="monthly")

[9]:

<Dual: 136.382058, (inflation0, inflation1, inflation2, ...), [-0.0, -0.0, -15.8, ...]>

[10]:

inflation_curve.index_value(dt(2027, 5, 15), index_lag=3, interpolation="monthly")

[10]:

<Dual: 135.763963, (inflation0, inflation1, inflation2, ...), [-0.0, -0.0, -38.9, ...]>

Seasonality#

The way rateslib handles seasonality is to replicate it via its CompositeCurve framework. If we create a Curve with nodes replicating factors we might create something like:

[11]:

seasonality = Curve(

nodes={

dt(2024, 4, 1): 1.0,

dt(2025, 3, 1): 1.0,

dt(2025, 4, 1): 1.0,

dt(2025, 5, 1): 1.0,

dt(2025, 6, 1): 1.0,

dt(2025, 7, 1): 1.0,

dt(2074, 5, 11): 1.0

},

convention="Act365F",

id="season"

)

solver_s2 = Solver(

curves=[seasonality],

instruments=[

Value(dt(2024, 4, 1), curves="season", metric="o/n_rate"),

Value(dt(2025, 3, 1), curves="season", metric="o/n_rate"),

Value(dt(2025, 4, 1), curves="season", metric="o/n_rate"),

Value(dt(2025, 5, 1), curves="season", metric="o/n_rate"),

Value(dt(2025, 6, 1), curves="season", metric="o/n_rate"),

Value(dt(2025, 7, 1), curves="season", metric="o/n_rate"),

],

s=[0.0, -0.3, 0.3, -0.4, 0.4, 0.0],

instrument_labels=["s0", "s1", "s2", "s3", "s4", "s5"],

id="seasonality",

)

SUCCESS: `func_tol` reached after 5 iterations (levenberg_marquardt), `f_val`: 6.966362122021486e-12, `time`: 0.0071s

[12]:

seasonality.plot("1b", right=dt(2026, 4, 1))

[12]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x10f34b4d0>])

[13]:

adjusted_inflation = CompositeCurve(curves=[inflation_curve, seasonality], id="adj_inflation")

adjusted_inflation.plot("1b", right=dt(2028, 1, 1))

[13]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x10f5dec10>])

[14]:

solver = Solver(

pre_solvers=[solver1, solver_s2],

curves=[adjusted_inflation, inflation_curve],

instruments=[

ZCIS(dt(2024, 5, 11), "1y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "2y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "3y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "4y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "5y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "7y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "10y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "12y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "15y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "20y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "25y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "30y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "40y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

ZCIS(dt(2024, 5, 11), "50y", spec="eur_zcis", curves=["adj_inflation", "discount"], leg2_index_fixings=fixings),

],

s=[2.93, 2.95, 2.965, 2.98, 3.0, 3.06, 3.175, 3.243, 3.293, 3.338, 3.348, 3.348, 3.308, 3.228],

instrument_labels=["1y", "2y", "3y", "4y", "5y", "7y", "10y", "12y", "15", "20y", "25y", "30y", "40y", "50y"],

id="zcis",

)

SUCCESS: `func_tol` reached after 4 iterations (levenberg_marquardt), `f_val`: 1.0300554017220054e-13, `time`: 0.0299s

We sample a few dates

[15]:

f1 = adjusted_inflation.index_value(dt(2025, 3, 1), index_lag=0)

f2 = adjusted_inflation.index_value(dt(2025, 4, 1), index_lag=0)

f3 = adjusted_inflation.index_value(dt(2025, 5, 1), index_lag=0)

f4 = adjusted_inflation.index_value(dt(2025, 6, 1), index_lag=0)

print(float(f1), float(f2), float(f3), float(f4))

128.19527824617822 128.36352410657304 128.58994830252666 128.8580493924425

These values compare to the underlying, non-seasonaility adjusted curves as follows:

[16]:

f1 = inflation_curve.index_value(dt(2025, 3, 1), index_lag=0)

f2 = inflation_curve.index_value(dt(2025, 4, 1), index_lag=0)

f3 = inflation_curve.index_value(dt(2025, 5, 1), index_lag=0)

f4 = inflation_curve.index_value(dt(2025, 6, 1), index_lag=0)

print(float(f1), float(f2), float(f3), float(f4))

128.1952781881416 128.39623301907898 128.5910053629069 128.9028908233816

The trick here is obviously to find a representation of a seasonaility curve that matches one’s expectation of seasonality adjustments. Here, a Solver calibration was used to separately solve the seasonality curve to inflation rate adjustments.

Inflation Swap and DV01#

We can easily construct a ZCIS or other type of inflation based instrument and use the native delta and gamma methods associated with a Solver to extract risk sensitivities.

[17]:

zcis = ZCIS(dt(2024, 3, 11), "4y", spec="eur_zcis", curves=["adj_inflation", "discount"], fixed_rate=3.0, leg2_index_fixings=fixings)

[18]:

zcis.rate(solver=solver)

[18]:

<Dual: 2.913238, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, 0.0, ...]>

[19]:

zcis.npv(solver=solver)

[19]:

<Dual: -3369.848948, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, 0.0, ...]>

[20]:

zcis.delta(solver=solver).style.format(precision=0)

[20]:

| local_ccy | eur | ||

|---|---|---|---|

| display_ccy | eur | ||

| type | solver | label | |

| instruments | rates | nominal | 1 |

| seasonality | s0 | -1 | |

| s1 | 0 | ||

| s2 | 0 | ||

| s3 | 0 | ||

| s4 | 0 | ||

| s5 | -0 | ||

| zcis | 1y | 4 | |

| 2y | -23 | ||

| 3y | 93 | ||

| 4y | 297 | ||

| 5y | -0 | ||

| 7y | 0 | ||

| 10y | 0 | ||

| 12y | 0 | ||

| 15 | 0 | ||

| 20y | -0 | ||

| 25y | -0 | ||

| 30y | -0 | ||

| 40y | -0 | ||

| 50y | -0 |

[21]:

zcis.gamma(solver=solver).style.format(precision=1)

[21]:

| type | instruments | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| solver | rates | seasonality | zcis | ||||||||||||||||||||||

| label | nominal | s0 | s1 | s2 | s3 | s4 | s5 | 1y | 2y | 3y | 4y | 5y | 7y | 10y | 12y | 15 | 20y | 25y | 30y | 40y | 50y | ||||

| local_ccy | display_ccy | type | solver | label | |||||||||||||||||||||

| eur | eur | instruments | rates | nominal | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.1 | 0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 |

| seasonality | s0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | |||

| s1 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | ||||

| s2 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | ||||

| s3 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | ||||

| s4 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | ||||

| s5 | 0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | ||||

| zcis | 1y | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | |||

| 2y | 0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | ||||

| 3y | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | ||||

| 4y | -0.1 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.1 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | ||||

| 5y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 7y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 10y | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 12y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 15 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 20y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 25y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 30y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 40y | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | ||||

| 50y | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | ||||