[1]:

from rateslib import *

Constructing Curves from (CC) Zero Rates#

A common type of curve definition in quantitative analysis is to construct a Curve from continuously compounded zero coupon rates.

There is a one-to-one equivalence relation between discount factors (DFs) and cc zero rates:

where \(d\) is the day count fraction (DCF) measured between ‘today’ and the ‘maturity’ date of the rate, using the convention assocoiated with the rates.

In rateslib a Curve is defined by DF nodes, so if one wants to construct a Curve from zero rates either these have to be manually converted to DFs or the Solver can be used to determine them via calibration.

Direct conversion#

Writing a manual conversion function is not difficult. We just need to use the above formula directly.

[2]:

def curve_from_zero_rates(nodes, convention, calendar):

start = list(nodes.keys())[0]

nodes_ = {

**{date: dual_exp(-dcf(start, date, convention=convention) * r/100.0)

for (date,r) in list(nodes.items())}

}

return Curve(nodes=nodes_, convention=convention, calendar=calendar)

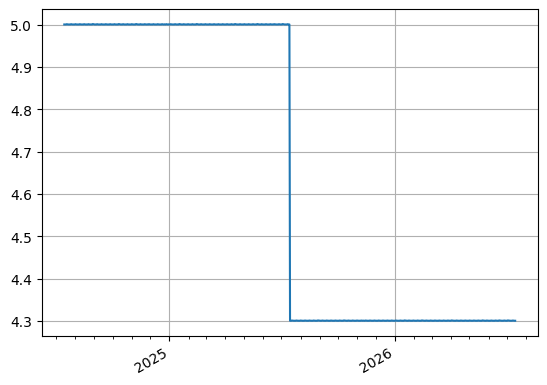

[3]:

curve = curve_from_zero_rates(

{dt(2024, 7, 15): 0.0, dt(2025, 7, 15): 5.00, dt(2026, 7, 15): 4.65},

convention="act365f",

calendar="nyc",

)

curve.plot("1d")

[3]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x115c216d0>])

[4]:

curve.nodes

[4]:

{datetime.datetime(2024, 7, 15, 0, 0): 1.0,

datetime.datetime(2025, 7, 15, 0, 0): 0.951229424500714,

datetime.datetime(2026, 7, 15, 0, 0): 0.9111935002961405}

If cubic spline interpolation was required this could be included within the curve_from_zero_rates function using the t argument from a Curve.

Using a Solver#

The advantage of using a Solver is that the Curve can be calibrated directly without a manually written construction function and derivatives and risk sensitivities are automatically obtained. The easiest way to directly specify this is to use the Value class.

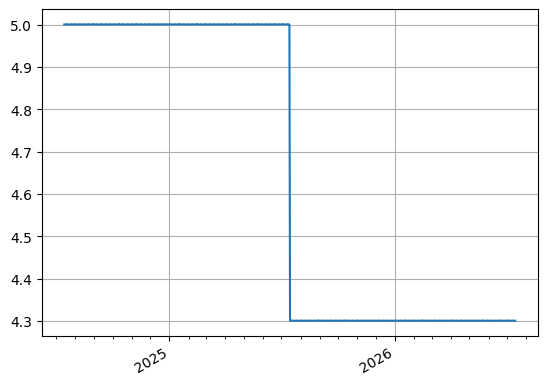

[5]:

curve = Curve(

{dt(2024, 7, 15): 1.0, dt(2025, 7, 15): 1.0, dt(2026, 7, 15): 1.0},

convention="act365f", calendar="nyc", id="ccz_curve"

)

solver = Solver(

curves=[curve],

instruments=[

Value(dt(2025, 7, 15), "act365f" ,metric="cc_zero_rate", curves=curve),

Value(dt(2026, 7, 15), "act365f" ,metric="cc_zero_rate", curves=curve),

],

s=[5.0, 4.65] # <- Same rates to observe same derived discount factors

)

SUCCESS: `func_tol` reached after 4 iterations (levenberg_marquardt), `f_val`: 7.99937338613464e-16, `time`: 0.0013s

[6]:

curve.plot("1d")

[6]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x115f1b110>])

[7]:

curve.nodes

[7]:

{datetime.datetime(2024, 7, 15, 0, 0): <Dual: 1.000000, (ccz_curve0, ccz_curve1, ccz_curve2), [1.0, 0.0, 0.0]>,

datetime.datetime(2025, 7, 15, 0, 0): <Dual: 0.951229, (ccz_curve0, ccz_curve1, ccz_curve2), [0.0, 1.0, 0.0]>,

datetime.datetime(2026, 7, 15, 0, 0): <Dual: 0.911194, (ccz_curve0, ccz_curve1, ccz_curve2), [0.0, 0.0, 1.0]>}