A EURUSD market for IRS, cross-currency and FX volatility#

In this notebook we demonstrate the code for rateslib to build:

local currency interest rate curves in EUR and USD from RFR swaps,

collateral curves accounting for the cross-currency basis and FX swap points,

volatility surface priced from FX volatility products.

Input market data#

First things first we need market data for the interest rates curves and forward FX curves. This data was observed on 28th May 2024.

[1]:

from rateslib import *

import numpy as np

from pandas import DataFrame

[2]:

fxr = FXRates({"eurusd": 1.0867}, settlement=dt(2024, 5, 30))

[3]:

mkt_data = DataFrame(

data=[['1w', 3.9035,5.3267,3.33,],

['2w', 3.9046,5.3257,6.37,],

['3w',3.8271,5.3232,9.83,],

['1m',3.7817,5.3191,13.78,],

['2m',3.7204,5.3232,30.04,],

['3m',3.667,5.3185,45.85,-2.5],

['4m',3.6252,5.3307,61.95,],

['5m',3.587,5.3098,78.1,],

['6m',3.5803,5.3109,94.25,-3.125],

['7m',3.5626,5.301,110.82,],

['8m',3.531,5.2768,130.45,],

['9m',3.5089,5.2614,145.6,-7.25],

['10m',3.4842,5.2412,162.05,],

['11m',3.4563,5.2144,178,],

['1y',3.4336,5.1936,None,-6.75],

['15m',3.3412,5.0729,None,-6.75],

['18m',3.2606,4.9694,None,-6.75],

['21m',3.1897,4.8797,None,-7.75],

['2y',3.1283,4.8022,None,-7.875],

['3y',2.9254,4.535,None,-9],

['4y',2.81,4.364,None,-10.125],

['5y',2.7252,4.256,None,-11.125],

['6y',2.6773,4.192,None,-12.125],

['7y',2.6541,4.151,None,-13],

['8y',2.6431,4.122,None,-13.625],

['9y',2.6466,4.103,None,-14.25],

['10y',2.6562,4.091,None,-14.875],

['12y',2.6835,4.084,None,-16.125],

['15y',2.7197,4.08,None,-17],

['20y',2.6849,4.04,None,-16],

['25y',2.6032,3.946,None,-12.75],

['30y',2.5217,3.847,None,-9.5]],

columns=["tenor", "estr", "sofr", "fx_swap", "xccy"],

)

mkt_data

[3]:

| tenor | estr | sofr | fx_swap | xccy | |

|---|---|---|---|---|---|

| 0 | 1w | 3.9035 | 5.3267 | 3.33 | NaN |

| 1 | 2w | 3.9046 | 5.3257 | 6.37 | NaN |

| 2 | 3w | 3.8271 | 5.3232 | 9.83 | NaN |

| 3 | 1m | 3.7817 | 5.3191 | 13.78 | NaN |

| 4 | 2m | 3.7204 | 5.3232 | 30.04 | NaN |

| 5 | 3m | 3.6670 | 5.3185 | 45.85 | -2.500 |

| 6 | 4m | 3.6252 | 5.3307 | 61.95 | NaN |

| 7 | 5m | 3.5870 | 5.3098 | 78.10 | NaN |

| 8 | 6m | 3.5803 | 5.3109 | 94.25 | -3.125 |

| 9 | 7m | 3.5626 | 5.3010 | 110.82 | NaN |

| 10 | 8m | 3.5310 | 5.2768 | 130.45 | NaN |

| 11 | 9m | 3.5089 | 5.2614 | 145.60 | -7.250 |

| 12 | 10m | 3.4842 | 5.2412 | 162.05 | NaN |

| 13 | 11m | 3.4563 | 5.2144 | 178.00 | NaN |

| 14 | 1y | 3.4336 | 5.1936 | NaN | -6.750 |

| 15 | 15m | 3.3412 | 5.0729 | NaN | -6.750 |

| 16 | 18m | 3.2606 | 4.9694 | NaN | -6.750 |

| 17 | 21m | 3.1897 | 4.8797 | NaN | -7.750 |

| 18 | 2y | 3.1283 | 4.8022 | NaN | -7.875 |

| 19 | 3y | 2.9254 | 4.5350 | NaN | -9.000 |

| 20 | 4y | 2.8100 | 4.3640 | NaN | -10.125 |

| 21 | 5y | 2.7252 | 4.2560 | NaN | -11.125 |

| 22 | 6y | 2.6773 | 4.1920 | NaN | -12.125 |

| 23 | 7y | 2.6541 | 4.1510 | NaN | -13.000 |

| 24 | 8y | 2.6431 | 4.1220 | NaN | -13.625 |

| 25 | 9y | 2.6466 | 4.1030 | NaN | -14.250 |

| 26 | 10y | 2.6562 | 4.0910 | NaN | -14.875 |

| 27 | 12y | 2.6835 | 4.0840 | NaN | -16.125 |

| 28 | 15y | 2.7197 | 4.0800 | NaN | -17.000 |

| 29 | 20y | 2.6849 | 4.0400 | NaN | -16.000 |

| 30 | 25y | 2.6032 | 3.9460 | NaN | -12.750 |

| 31 | 30y | 2.5217 | 3.8470 | NaN | -9.500 |

Solving rates curves and FX forwards curve#

We will create all Curves and solve them all using the Solver. It is possible to solve everything simultaneously in a single Solver but this is less efficient than decoupling the known separable components, and using multiple Solvers in a dependency chain.

[4]:

eur = Curve(

nodes={

dt(2024, 5, 28): 1.0,

**{add_tenor(dt(2024, 5, 30), _, "F", "tgt"): 1.0 for _ in mkt_data["tenor"]}

},

calendar="tgt",

interpolation="log_linear",

convention="act360",

id="estr",

)

usd = Curve(

nodes={

dt(2024, 5, 28): 1.0,

**{add_tenor(dt(2024, 5, 30), _, "F", "nyc"): 1.0 for _ in mkt_data["tenor"]}

},

calendar="nyc",

interpolation="log_linear",

convention="act360",

id="sofr",

)

eurusd = Curve(

nodes={

dt(2024, 5, 28): 1.0,

**{add_tenor(dt(2024, 5, 30), _, "F", "tgt"): 1.0 for _ in mkt_data["tenor"]}

},

interpolation="log_linear",

convention="act360",

id="eurusd",

)

With Curves created but not necessarily calibrated we can design the FXForwards market mapping:

[5]:

fxf = FXForwards(

fx_rates=fxr,

fx_curves={"eureur": eur, "eurusd": eurusd, "usdusd": usd}

)

The Instruments used to solve the ESTR curve are ESTR swaps and the SOFR curve are SOFR swaps:

[6]:

estr_swaps = [IRS(dt(2024, 5, 30), _, spec="eur_irs", curves="estr") for _ in mkt_data["tenor"]]

estr_rates = mkt_data["estr"].tolist()

labels = mkt_data["tenor"].to_list()

sofr_swaps = [IRS(dt(2024, 5, 30), _, spec="usd_irs", curves="sofr") for _ in mkt_data["tenor"]]

sofr_rates = mkt_data["sofr"].tolist()

[7]:

eur_solver = Solver(

curves=[eur],

instruments=estr_swaps,

s=estr_rates,

fx=fxf,

instrument_labels=labels,

id="eur",

)

usd_solver = Solver(

curves=[usd],

instruments=sofr_swaps,

s=sofr_rates,

fx=fxf,

instrument_labels=labels,

id="usd",

)

SUCCESS: `func_tol` reached after 7 iterations (levenberg_marquardt), `f_val`: 1.6125193535364693e-15, `time`: 0.2175s

SUCCESS: `func_tol` reached after 7 iterations (levenberg_marquardt), `f_val`: 3.993407065375496e-17, `time`: 0.2185s

The cross currency curve use a combination of FXSwaps and XCS:

[8]:

fxswaps = [FXSwap(dt(2024, 5, 30), _, pair="eurusd", curves=[None, "eurusd", None, "sofr"]) for _ in mkt_data["tenor"][0:14]]

fxswap_rates = mkt_data["fx_swap"][0:14].tolist()

xcs = [XCS(dt(2024, 5, 30), _, spec="eurusd_xcs", curves=["estr", "eurusd", "sofr", "sofr"]) for _ in mkt_data["tenor"][14:]]

xcs_rates = mkt_data["xccy"][14:].tolist()

[9]:

fx_solver = Solver(

pre_solvers=[eur_solver, usd_solver],

curves=[eurusd],

instruments=fxswaps + xcs,

s=fxswap_rates + xcs_rates,

fx=fxf,

instrument_labels=labels,

id="eurusd_xccy",

)

SUCCESS: `func_tol` reached after 5 iterations (levenberg_marquardt), `f_val`: 2.660105897983944e-21, `time`: 2.0243s

Solving an FX Vol Surface#

Next we will use the market FX volatility quotes to build a surface. These prices are all expressed in log-normal vol terms under normal market conventions and the instruments 1Y or less use spot unadjusted delta and those longer than 1y use forward undajusted delta.

[10]:

vol_data = DataFrame(

data=[

['1w',4.535,-0.047,0.07,-0.097,0.252],

['2w',5.168,-0.082,0.077,-0.165,0.24],

['3w',5.127,-0.175,0.07,-0.26,0.233],

['1m',5.195,-0.2,0.07,-0.295,0.235],

['2m',5.237,-0.28,0.087,-0.535,0.295],

['3m',5.257,-0.363,0.1,-0.705,0.35],

['4m',5.598,-0.47,0.123,-0.915,0.422],

['5m',5.776,-0.528,0.133,-1.032,0.463],

['6m',5.92,-0.565,0.14,-1.11,0.49],

['9m',6.01,-0.713,0.182,-1.405,0.645],

['1y',6.155,-0.808,0.23,-1.585,0.795],

['18m',6.408,-0.812,0.248,-1.588,0.868],

['2y',6.525,-0.808,0.257,-1.58,0.9],

['3y',6.718,-0.733,0.265,-1.45,0.89],

['4y',7.025,-0.665,0.265,-1.31,0.885],

['5y',7.26,-0.62,0.26,-1.225,0.89],

['6y',7.508,-0.516,0.27,-0.989,0.94],

['7y',7.68,-0.442,0.278,-0.815,0.975],

['10y',8.115,-0.267,0.288,-0.51,1.035],

['15y',8.652,-0.325,0.362,-0.4,1.195],

['20y',8.651,-0.078,0.343,-0.303,1.186],

['25y',8.65,-0.029,0.342,-0.218,1.178],

['30y',8.65,0.014,0.341,-0.142,1.171],

],

columns=["tenor", "atm", "25drr", "25dbf", "10drr", "10dbf"]

)

vol_data["expiry"] = [add_tenor(dt(2024, 5, 28), _, "MF", "tgt") for _ in vol_data["tenor"]]

vol_data

[10]:

| tenor | atm | 25drr | 25dbf | 10drr | 10dbf | expiry | |

|---|---|---|---|---|---|---|---|

| 0 | 1w | 4.535 | -0.047 | 0.070 | -0.097 | 0.252 | 2024-06-04 |

| 1 | 2w | 5.168 | -0.082 | 0.077 | -0.165 | 0.240 | 2024-06-11 |

| 2 | 3w | 5.127 | -0.175 | 0.070 | -0.260 | 0.233 | 2024-06-18 |

| 3 | 1m | 5.195 | -0.200 | 0.070 | -0.295 | 0.235 | 2024-06-28 |

| 4 | 2m | 5.237 | -0.280 | 0.087 | -0.535 | 0.295 | 2024-07-29 |

| 5 | 3m | 5.257 | -0.363 | 0.100 | -0.705 | 0.350 | 2024-08-28 |

| 6 | 4m | 5.598 | -0.470 | 0.123 | -0.915 | 0.422 | 2024-09-30 |

| 7 | 5m | 5.776 | -0.528 | 0.133 | -1.032 | 0.463 | 2024-10-28 |

| 8 | 6m | 5.920 | -0.565 | 0.140 | -1.110 | 0.490 | 2024-11-28 |

| 9 | 9m | 6.010 | -0.713 | 0.182 | -1.405 | 0.645 | 2025-02-28 |

| 10 | 1y | 6.155 | -0.808 | 0.230 | -1.585 | 0.795 | 2025-05-28 |

| 11 | 18m | 6.408 | -0.812 | 0.248 | -1.588 | 0.868 | 2025-11-28 |

| 12 | 2y | 6.525 | -0.808 | 0.257 | -1.580 | 0.900 | 2026-05-28 |

| 13 | 3y | 6.718 | -0.733 | 0.265 | -1.450 | 0.890 | 2027-05-28 |

| 14 | 4y | 7.025 | -0.665 | 0.265 | -1.310 | 0.885 | 2028-05-29 |

| 15 | 5y | 7.260 | -0.620 | 0.260 | -1.225 | 0.890 | 2029-05-28 |

| 16 | 6y | 7.508 | -0.516 | 0.270 | -0.989 | 0.940 | 2030-05-28 |

| 17 | 7y | 7.680 | -0.442 | 0.278 | -0.815 | 0.975 | 2031-05-28 |

| 18 | 10y | 8.115 | -0.267 | 0.288 | -0.510 | 1.035 | 2034-05-29 |

| 19 | 15y | 8.652 | -0.325 | 0.362 | -0.400 | 1.195 | 2039-05-30 |

| 20 | 20y | 8.651 | -0.078 | 0.343 | -0.303 | 1.186 | 2044-05-30 |

| 21 | 25y | 8.650 | -0.029 | 0.342 | -0.218 | 1.178 | 2049-05-28 |

| 22 | 30y | 8.650 | 0.014 | 0.341 | -0.142 | 1.171 | 2054-05-28 |

A Surface is defined by given expiries and delta grdipoints. All vol values are initially set to 5.0, and will be calibrated by the Instruments.

[11]:

surface = FXDeltaVolSurface(

eval_date=dt(2024, 5, 28),

expiries=vol_data["expiry"],

delta_indexes=[0.1, 0.25, 0.5, 0.75, 0.9],

node_values=np.ones((23, 5))*5.0,

delta_type="forward",

id="eurusd_vol"

)

Define the instruments and their rates for 1Y or less:

[12]:

fx_args = dict(

pair="eurusd",

curves=[None, "eurusd", None, "sofr"],

calendar="tgt",

delivery_lag=2,

payment_lag=2,

eval_date=dt(2024, 5, 28),

modifier="MF",

premium_ccy="usd",

vol="eurusd_vol",

)

instruments_le_1y, rates_le_1y, labels_le_1y = [], [], []

for row in range(11):

instruments_le_1y.extend([

FXStraddle(strike="atm_delta", expiry=vol_data["expiry"][row], delta_type="spot", **fx_args),

FXRiskReversal(strike=["-25d", "25d"], expiry=vol_data["expiry"][row], delta_type="spot", **fx_args),

FXBrokerFly(strike=["-25d", "atm_delta", "25d"], expiry=vol_data["expiry"][row], delta_type="spot", **fx_args),

FXRiskReversal(strike=["-10d", "10d"], expiry=vol_data["expiry"][row], delta_type="spot", **fx_args),

FXBrokerFly(strike=["-10d", "atm_delta", "10d"], expiry=vol_data["expiry"][row], delta_type="spot", **fx_args),

])

rates_le_1y.extend([vol_data["atm"][row], vol_data["25drr"][row], vol_data["25dbf"][row], vol_data["10drr"][row], vol_data["10dbf"][row]])

labels_le_1y.extend([f"atm_{row}", f"25drr_{row}", f"25dbf_{row}", f"10drr_{row}", f"10dbf_{row}"])

Also define the instruments and rates for greater than 1Y:

[13]:

instruments_gt_1y, rates_gt_1y, labels_gt_1y = [], [], []

for row in range(11, 23):

instruments_gt_1y.extend([

FXStraddle(strike="atm_delta", expiry=vol_data["expiry"][row], delta_type="forward", **fx_args),

FXRiskReversal(strike=["-25d", "25d"], expiry=vol_data["expiry"][row], delta_type="forward", **fx_args),

FXBrokerFly(strike=["-25d", "atm_delta", "25d"], expiry=vol_data["expiry"][row], delta_type="forward", **fx_args),

FXRiskReversal(strike=["-10d", "10d"], expiry=vol_data["expiry"][row], delta_type="forward", **fx_args),

FXBrokerFly(strike=["-10d", "atm_delta", "10d"], expiry=vol_data["expiry"][row], delta_type="forward", **fx_args),

])

rates_gt_1y.extend([vol_data["atm"][row], vol_data["25drr"][row], vol_data["25dbf"][row], vol_data["10drr"][row], vol_data["10dbf"][row]])

labels_gt_1y.extend([f"atm_{row}", f"25drr_{row}", f"25dbf_{row}", f"10drr_{row}", f"10dbf_{row}"])

Now solve for all calibrating instruments and rates.

[14]:

surface_solver = Solver(

surfaces=[surface],

instruments=instruments_le_1y+instruments_gt_1y,

s=rates_le_1y+rates_gt_1y,

instrument_labels=labels_le_1y+labels_gt_1y,

fx=fxf,

pre_solvers=[fx_solver],

id="eurusd_vol"

)

SUCCESS: `func_tol` reached after 14 iterations (levenberg_marquardt), `f_val`: 9.091299248723455e-13, `time`: 5.7012s

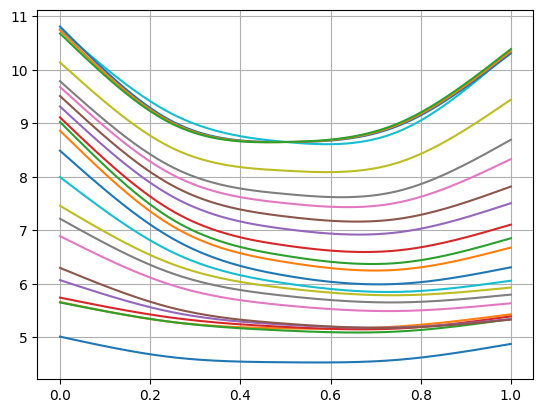

3D Surface Plot and Cross-sectional Smiles#

[15]:

surface.plot()

[15]:

(<Figure size 640x480 with 1 Axes>, <Axes3D: >, None)

[16]:

surface.smiles[0].plot(comparators=surface.smiles[1:])

[16]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x113b5efd0>,

<matplotlib.lines.Line2D at 0x113b5f110>,

<matplotlib.lines.Line2D at 0x113b5f250>,

<matplotlib.lines.Line2D at 0x113b5f390>,

<matplotlib.lines.Line2D at 0x113b5f4d0>,

<matplotlib.lines.Line2D at 0x113b5f610>,

<matplotlib.lines.Line2D at 0x113b5f750>,

<matplotlib.lines.Line2D at 0x113b5f890>,

<matplotlib.lines.Line2D at 0x113b5f9d0>,

<matplotlib.lines.Line2D at 0x113b5fb10>,

<matplotlib.lines.Line2D at 0x113b5fc50>,

<matplotlib.lines.Line2D at 0x113b5fd90>,

<matplotlib.lines.Line2D at 0x113b5fed0>,

<matplotlib.lines.Line2D at 0x113ba0050>,

<matplotlib.lines.Line2D at 0x113ba0190>,

<matplotlib.lines.Line2D at 0x113ba02d0>,

<matplotlib.lines.Line2D at 0x113ba0410>,

<matplotlib.lines.Line2D at 0x113ba0550>,

<matplotlib.lines.Line2D at 0x113ba0690>,

<matplotlib.lines.Line2D at 0x113ba07d0>,

<matplotlib.lines.Line2D at 0x113ba0910>,

<matplotlib.lines.Line2D at 0x113ba0a50>,

<matplotlib.lines.Line2D at 0x113ba0b90>])

Calculating a generic option price#

[ ]: