User Guide#

Where to start?#

Rateslib tends to follow the typical quant architecture:

This means that financial instrument specification, curve and/or surface construction from market data including foreign exchange (FX) will permit pricing metrics and risk sensitivity. These functionalities are interlinked and potentially dependent upon each other. This guide will introduce them in a structured way and give typical examples how they are used in practice.

Let’s start with some fundamental Curve and Instrument constructors.

Trivial derivatives examples#

Rateslib has two fundamental Curve types. Most of the time you

will only need to use a Curve.

A Curve is discount factor (DF) based and is constructed

by providing DFs on specific node dates. Interpolation between nodes is

configurable, but the below uses the “log-linear” default.

In [1]: from rateslib import *

In [2]: usd_curve = Curve(

...: nodes={

...: dt(2022, 1, 1): 1.0,

...: dt(2022, 7, 1): 0.98,

...: dt(2023, 1, 1): 0.95

...: },

...: calendar="nyc",

...: id="sofr",

...: )

...:

A LineCurve is value based and is constructed

by providing curve values on specific node dates. Interpolation between nodes is

configurable, with the default being “linear” interpolation (hence LineCurve). This type

has no DFs so can’t be used for discounting cashflows.

In [3]: usd_legacy_3mIBOR = LineCurve(

...: nodes={

...: dt(2022, 1, 1): 2.635,

...: dt(2022, 7, 1): 2.896,

...: dt(2023, 1, 1): 2.989,

...: },

...: calendar="nyc",

...: id="us_ibor_3m",

...: )

...:

An Index Curve is required by certain products, e.g.

inflation linked bonds (IndexFixedRateBond) or

zero coupon inflation swaps (ZCIS). Adding index_base

and index_lag argument inputs extends a DF based Curve to

work in these cases.

In [4]: usd_cpi = Curve(

...: nodes={

...: dt(2022, 1, 1): 1.00,

...: dt(2022, 7, 1): 0.97,

...: dt(2023, 1, 1): 0.955,

...: },

...: index_base=308.95,

...: index_lag=3,

...: interpolation="linear_index",

...: id="us_cpi",

...: )

...:

A Hazard Curve is used by credit Instruments when a default is possible. Hazard Curves

utilise the same Curve class and the rates reflect overnight

hazard rates and the DFs reflect survival probabilities.

In [5]: pfizer_hazard = Curve(

...: nodes={

...: dt(2022, 1, 1): 1.0,

...: dt(2022, 7, 1): 0.998,

...: dt(2023, 1, 1): 0.995

...: },

...: id="pfizer_hazard",

...: credit_recovery_rate=0.4,

...: credit_discretization=23,

...: )

...:

Next, we will construct some basic derivative Instruments. These will use some market conventions defined by rateslib through its default argument specifications, although all arguments can be supplied manually if and when required.

Here we create a short dated SOFR RFR interest rate swap (IRS).

In [6]: irs = IRS(

...: effective=dt(2022, 2, 15),

...: termination="6m",

...: notional=1000000000,

...: fixed_rate=2.0,

...: spec="usd_irs"

...: )

...:

Here we create a SOFR STIR future (STIRFuture).

In [7]: stir = STIRFuture(

...: effective=get_imm(code="H22"),

...: termination=get_imm(code="M22"),

...: contracts=100,

...: price=97.495,

...: spec="usd_stir",

...: )

...:

A US LIBOR FRA is an obsolete Instrument, but we can still

create one and these still trade in other currencies, e.g. EUR.

In [8]: fra = FRA(

...: effective=dt(2022, 2, 16),

...: termination="3m",

...: frequency="Q",

...: calendar="nyc",

...: convention="act360",

...: leg2_method_param=2,

...: fixed_rate=2.5

...: )

...:

Here we construct a generic US investment grade credit default

swap (CDS)

In [9]: cds = CDS(

...: effective=dt(2021, 12, 20),

...: termination=dt(2022, 9, 20),

...: notional=15e6,

...: spec="us_ig_cds",

...: )

...:

This constructs a zero-coupon inflation swap

(ZCIS) with usual

daily index interpolation and 3-month index lag.

In [10]: zcis = ZCIS(

....: effective=dt(2022, 2, 2),

....: termination="9m",

....: notional=-25e6,

....: fixed_rate=3.25,

....: spec="usd_zcis",

....: )

....:

We can combine the Curves and the Instruments to give pricing metrics such as

npv(),

cashflows(), and the mid-market

rate(), as well as others. Without further specification

these values are all expressed in the Instrument’s local USD settlement currency.

In [11]: irs.npv(curves=usd_curve)

Out[11]: 12629097.829705866

In [12]: irs.cashflows(curves=usd_curve)

Out[12]:

Type Ccy Payment Notional Period Convention DCF Acc Start Acc End DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Rate Spread

leg1 0 FixedPeriod USD 2022-08-17 1000000000.00 Stub Act360 0.50 2022-02-15 2022-08-15 0.97 -10055555.56 -9776494.15 1.00 USD -9776494.15 None 2.00 NaN

leg2 0 FloatPeriod USD 2022-08-17 -1000000000.00 Stub Act360 0.50 2022-02-15 2022-08-15 0.97 23045139.84 22405591.98 1.00 USD 22405591.98 None 4.58 0.00

In [13]: stir.npv(curves=usd_curve)

Out[13]: -383423.5359790483

In [14]: stir.rate(curves=usd_curve, metric="price")

Out[14]: 95.96130585608381

In [15]: fra.npv(curves=[usd_legacy_3mIBOR, usd_curve])

Out[15]: 484.85927030340326

In [16]: fra.rate(curves=[usd_legacy_3mIBOR, usd_curve])

Out[16]: 2.698447513812155

In [17]: cds.npv(curves=[pfizer_hazard, usd_curve])

Out[17]: -82285.89860611843

In [18]: cds.rate(curves=[pfizer_hazard, usd_curve])

Out[18]: 0.26322526465564466

In [19]: cds.cashflows(curves=[pfizer_hazard, usd_curve])

Out[19]:

Type Ccy Payment Notional Period Convention DCF Acc Start Acc End Rate Spread DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Survival Recovery

leg1 0 CreditPremiumPeriod USD 2022-03-21 15000000.00 Regular Act360 0.25 2021-12-20 2022-03-21 1.00 None 0.99 -37916.67 -37569.55 1.00 USD -37569.55 None 1.00 0.40

1 CreditPremiumPeriod USD 2022-06-21 15000000.00 Regular Act360 0.26 2022-03-21 2022-06-21 1.00 None 0.98 -38333.33 -37556.66 1.00 USD -37556.66 None 1.00 0.40

2 CreditPremiumPeriod USD 2022-09-20 15000000.00 Regular Act360 0.25 2022-06-21 2022-09-20 1.00 None 0.97 -37916.67 -36557.72 1.00 USD -36557.72 None 1.00 0.40

leg2 0 CreditProtectionPeriod USD 2022-09-20 -15000000.00 Stub Act360 0.76 2021-12-20 2022-09-20 NaN NaN 0.97 9000000.00 29398.03 1.00 USD 29398.03 None 1.00 0.40

In [20]: zcis.npv(curves=[usd_cpi, usd_curve])

Out[20]: -285438.4728524148

In [21]: zcis.rate(curves=[usd_cpi, usd_curve])

Out[21]: 4.852119618886386

In [22]: zcis.cashflows(curves=[usd_cpi, usd_curve])

Out[22]:

Type Ccy Payment Notional Period Convention DCF Acc Start Acc End DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Rate Spread Index Base Index Val Index Ratio Index Fix Date Unindexed Cashflow

leg1 0 ZeroFixedPeriod USD 2022-11-02 -25000000.00 Stub YearsMonths 0.75 2022-02-02 2022-11-02 0.96 606932.34 582461.01 1.00 USD 582461.01 None 3.25 None NaN NaN NaN NaT NaN

leg2 0 Cashflow USD 2022-11-02 25000000.00 NaN NaN NaN NaT NaT 0.96 -904363.13 -867899.49 1.00 USD -867899.49 None NaN NaN 310.64 321.88 1.04 2022-11-02 -25000000.00

Securities and bonds#

Rateslib is steadily building a collection of market conventions for a host of global bonds. Again these specifications are available at default argument specifications for those that have already been populated.

A very common instrument in financial investing is a FixedRateBond.

At time of writing the on-the-run 10Y US treasury was the 3.875% Aug 2033 bond. Here we

construct this using the street convention and derive the price from yield-to-maturity and

risk calculations.

In [23]: fxb = FixedRateBond(

....: effective=dt(2023, 8, 15),

....: termination=dt(2033, 8, 15),

....: fixed_rate=3.875,

....: spec="us_gb" # US Government Bond

....: )

....:

In [24]: fxb.accrued(settlement=dt(2025, 2, 14))

Out[24]: 1.9269701086956519

In [25]: fxb.price(ytm=4.0, settlement=dt(2025, 2, 14))

Out[25]: 99.10641380057267

In [26]: fxb.duration(ytm=4.0, settlement=dt(2025, 2, 14), metric="duration")

Out[26]: np.float64(7.178560455252011)

In [27]: fxb.duration(ytm=4.0, settlement=dt(2025, 2, 14), metric="modified")

Out[27]: np.float64(7.037804367894129)

In [28]: fxb.duration(ytm=4.0, settlement=dt(2025, 2, 14), metric="risk")

Out[28]: np.float64(7.11053190579773)

A FloatRateNote can also be constructed. The below bond

settles to 3M-TermSOFR which is an IBOR style term fixing_method (and we simulate

its pricing with the Curves already constructed). Compounded RFR

FRNs can also be constructed, using other method inputs.

In [29]: frn = FloatRateNote(

....: effective=dt(2021, 8, 15),

....: termination=dt(2022, 8, 15),

....: frequency="Q",

....: float_spread=86.0,

....: spread_compound_method="none_simple",

....: convention="act360",

....: calendar="nyc",

....: payment_lag=0,

....: fixing_method="ibor",

....: method_param=0, # fixing lag is 0 business days

....: rate_fixings=[2.00, 2.14],

....: ex_div=1,

....: settle=1,

....: currency="usd",

....: )

....:

In [30]: frn.accrued(settlement=dt(2022, 1, 2))

Out[30]: 0.3999999999999999

In [31]: frn.rate(curves=[usd_legacy_3mIBOR, usd_curve])

Out[31]: 99.41819186149803

In [32]: frn.cashflows(curves=[usd_legacy_3mIBOR, usd_curve])

Out[32]:

Type Ccy Payment Notional Period Convention DCF Acc Start Acc End DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Rate Spread

leg1 0 FloatPeriod USD 2021-11-15 1000000.00 Regular Act360 0.25 2021-08-16 2021-11-15 0.00 -7229.44 0.00 1.00 USD 0.00 None 2.86 86.00

1 FloatPeriod USD 2022-02-15 1000000.00 Regular Act360 0.26 2021-11-15 2022-02-15 0.99 -7666.67 -7628.26 1.00 USD -7628.26 None 3.00 86.00

2 FloatPeriod USD 2022-05-16 1000000.00 Regular Act360 0.25 2022-02-15 2022-05-16 0.99 -8899.72 -8766.63 1.00 USD -8766.63 None 3.56 86.00

3 FloatPeriod USD 2022-08-15 1000000.00 Regular Act360 0.25 2022-05-16 2022-08-15 0.97 -9326.66 -9070.89 1.00 USD -9070.89 None 3.69 86.00

4 Cashflow USD 2022-08-15 1000000.00 NaN NaN NaN NaT NaT 0.97 -1000000.00 -972576.66 1.00 USD -972576.66 None NaN NaN

Below we construct a US government bond Bill using

default spec.

In [33]: bill = Bill(

....: effective=dt(2024, 10, 24),

....: termination=dt(2025, 4, 24),

....: spec="us_gbb", # US Government Bond-Bill

....: )

....:

In [34]: bill.discount_rate(price=99.0808021, settlement=dt(2025, 2, 4))

Out[34]: 4.188749924050641

In [35]: bill.ytm(price=99.0808021, settlement=dt(2025, 2, 4))

Out[35]: 4.300459677867501

In [36]: bill.duration(ytm=4.18875, settlement=dt(2025, 2, 4), metric="risk")

Out[36]: np.float64(0.21944444444444444)

In [37]: bill.price(rate=4.18875, settlement=dt(2025, 2, 4))

Out[37]: 99.08080208333334

Below we construct an IndexFixedRateBond, using relevant

indexing arguments.

In [38]: ifrb = IndexFixedRateBond( # CUSIP:91282CCA7 ISIN:US91282CCA71

....: effective=dt(2021, 4, 15),

....: termination=dt(2026, 4, 15),

....: fixed_rate=0.125,

....: index_base=262.250270,

....: index_fixings=265.0,

....: spec="us_gbi",

....: )

....:

In [39]: ifrb.price(ytm=1.397926, settlement=dt(2025, 2, 4))

Out[39]: 98.49999982402322

In [40]: ifrb.accrued(settlement=dt(2025, 2, 4))

Out[40]: 0.038461538461538464

In [41]: ifrb.cashflows(curves=[usd_cpi, usd_curve])

Out[41]:

Type Ccy Payment Notional Period Convention DCF Acc Start Acc End DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Rate Spread Index Base Index Val Index Ratio Index Fix Date Unindexed Cashflow

leg1 0 FixedPeriod USD 2021-10-15 1000000.00 Regular ActActICMA 0.50 2021-04-15 2021-10-15 0.00 -631.55 0.00 1.00 USD 0.00 None 0.12 NaN 262.25 265.00 1.01 2021-10-15 -625.00

1 FixedPeriod USD 2022-04-18 1000000.00 Regular ActActICMA 0.50 2021-10-15 2022-04-15 0.99 -749.38 -740.48 1.00 USD -740.48 None 0.12 NaN 262.25 314.44 1.20 2022-04-15 -625.00

2 FixedPeriod USD 2022-10-17 1000000.00 Regular ActActICMA 0.50 2022-04-15 2022-10-15 0.96 -765.94 -737.04 1.00 USD -737.04 None 0.12 NaN 262.25 321.39 1.23 2022-10-15 -625.00

3 FixedPeriod USD 2023-04-17 1000000.00 Regular ActActICMA 0.50 2022-10-15 2023-04-15 0.93 -777.73 -725.73 1.00 USD -725.73 None 0.12 NaN 262.25 326.34 1.24 2023-04-15 -625.00

4 FixedPeriod USD 2023-10-16 1000000.00 Regular ActActICMA 0.50 2023-04-15 2023-10-15 0.90 -789.59 -714.48 1.00 USD -714.48 None 0.12 NaN 262.25 331.31 1.26 2023-10-15 -625.00

5 FixedPeriod USD 2024-04-15 1000000.00 Regular ActActICMA 0.50 2023-10-15 2024-04-15 0.88 -801.44 -703.25 1.00 USD -703.25 None 0.12 NaN 262.25 336.29 1.28 2024-04-15 -625.00

6 FixedPeriod USD 2024-10-15 1000000.00 Regular ActActICMA 0.50 2024-04-15 2024-10-15 0.85 -813.30 -691.92 1.00 USD -691.92 None 0.12 NaN 262.25 341.26 1.30 2024-10-15 -625.00

7 FixedPeriod USD 2025-04-15 1000000.00 Regular ActActICMA 0.50 2024-10-15 2025-04-15 0.82 -825.10 -680.70 1.00 USD -680.70 None 0.12 NaN 262.25 346.21 1.32 2025-04-15 -625.00

8 FixedPeriod USD 2025-10-15 1000000.00 Regular ActActICMA 0.50 2025-04-15 2025-10-15 0.80 -836.95 -669.45 1.00 USD -669.45 None 0.12 NaN 262.25 351.19 1.34 2025-10-15 -625.00

9 FixedPeriod USD 2026-04-15 1000000.00 Regular ActActICMA 0.50 2025-10-15 2026-04-15 0.78 -848.75 -658.33 1.00 USD -658.33 None 0.12 NaN 262.25 356.13 1.36 2026-04-15 -625.00

10 Cashflow USD 2026-04-15 1000000.00 NaN NaN NaN NaT NaT 0.78 -1357993.45 -1053323.30 1.00 USD -1053323.30 None NaN NaN 262.25 356.13 1.36 2026-04-15 -1000000.00

There are some interesting Cookbook articles

on BondFuture and cheapest-to-deliver (CTD) analysis.

Quick look at FX#

Spot rates and conversion#

The above values were all calculated and displayed in USD. That is the default

currency in rateslib and the local currency of those Instruments. We can convert these values

into another currency using the FXRates class. This is a basic class which is

parametrised by some exchange rates.

In [42]: fxr = FXRates({"eurusd": 1.05, "gbpusd": 1.25})

In [43]: fxr.rates_table()

Out[43]:

usd eur gbp

usd 1.00 0.95 0.80

eur 1.05 1.00 0.84

gbp 1.25 1.19 1.00

We now have a mechanism by which to specify values in other currencies.

In [44]: irs.npv(curves=usd_curve, fx=fxr, base="usd")

Out[44]: 12629097.829705866

In [45]: irs.npv(curves=usd_curve, fx=fxr, base="eur")

Out[45]: <Dual: 12027712.218767, (fx_eurusd), [-11454964.0]>

In [46]: stir.npv(curves=usd_curve, fx=fxr, base="usd")

Out[46]: -383423.5359790483

In [47]: stir.npv(curves=usd_curve, fx=fxr, base="eur")

Out[47]: <Dual: -365165.272361, (fx_eurusd), [347776.4]>

In [48]: fra.npv(curves=[usd_legacy_3mIBOR, usd_curve], fx=fxr, base="usd")

Out[48]: 484.85927030340326

In [49]: fra.npv(curves=[usd_legacy_3mIBOR, usd_curve], fx=fxr, base="eur")

Out[49]: <Dual: 461.770734, (fx_eurusd), [-439.8]>

In [50]: cds.npv(curves=[pfizer_hazard, usd_curve], fx=fxr, base="usd")

Out[50]: -82285.89860611843

In [51]: cds.npv(curves=[pfizer_hazard, usd_curve], fx=fxr, base="eur")

Out[51]: <Dual: -78367.522482, (fx_eurusd), [74635.7]>

In [52]: zcis.npv(curves=[usd_cpi, usd_curve], fx=fxr, base="usd")

Out[52]: -285438.4728524148

In [53]: zcis.npv(curves=[usd_cpi, usd_curve], fx=fxr, base="eur")

Out[53]: <Dual: -271846.164621, (fx_eurusd), [258901.1]>

One observes that the value returned here is not a float but a Dual

which is part of rateslib’s AD framework. This is the first example of capturing a

sensitivity, which here denotes the sensitivity of the EUR NPV relative to the EURUSD FX rate.

One can read more about this particular treatment of FX

here and more generally about the dual AD framework here.

FX forwards#

For multi-currency derivatives we need more than basic, spot exchange rates.

We need an FXForwards market.

This stores the FX rates and the interest

rates curves that are used for all the FX-interest rate parity derivations. With these

we can calculate forward FX rates and also ad-hoc FX swap rates.

When defining the fx_curves dict mapping, the key “eurusd” should be interpreted as; the

Curve for EUR cashflows, collateralised in USD, and similarly for other entries.

In [54]: eur_curve = Curve({

....: dt(2022, 1, 1): 1.0,

....: dt(2022, 7, 1): 0.972,

....: dt(2023, 1, 1): 0.98},

....: calendar="tgt",

....: )

....:

In [55]: eurusd_curve = Curve({

....: dt(2022, 1, 1): 1.0,

....: dt(2022, 7, 1): 0.973,

....: dt(2023, 1, 1): 0.981}

....: )

....:

In [56]: fxf = FXForwards(

....: fx_rates=FXRates({"eurusd": 1.05}, settlement=dt(2022, 1, 1)),

....: fx_curves={

....: "usdusd": usd_curve,

....: "eureur": eur_curve,

....: "eurusd": eurusd_curve,

....: }

....: )

....:

In [57]: fxf.rate("eurusd", settlement=dt(2023, 1, 1))

Out[57]: <Dual: 1.084263, (fx_eurusd), [1.0]>

In [58]: fxf.swap("eurusd", settlements=[dt(2022, 2, 1), dt(2022, 5, 2)])

Out[58]: <Dual: -37.314180, (fx_eurusd), [-35.5]>

FXForwards objects are comprehensive and more information regarding all of the FX features is available in this link.

More about instruments#

We’ve seen some single currency derivatives above. A complete guide for all of the Instruments is available in this link. That will also introduce the building blocks; Legs and Periods.

Multi-currency instruments#

Let’s take a look at the multi-currency instruments. Notice how these Instruments

maintain consistent method naming conventions with those above. This makes it possible to plug

any Instruments into a Solver to calibrate Curves

around target mid-market rates, and generate market risks.

This is an FXSwap.

In [59]: fxs = FXSwap(

....: effective=dt(2022, 2, 1),

....: termination="3m", # May-1 is a holiday, May-2 is business end date.

....: pair="eurusd",

....: notional=20e6,

....: calendar="tgt|fed",

....: )

....:

In [60]: fxs.rate(curves=[eurusd_curve, usd_curve], fx=fxf)

Out[60]: <Dual: -37.314180, (fx_eurusd), [-35.5]>

In [61]: fxs.cashflows_table(curves=[eurusd_curve, usd_curve], fx=fxf)

Out[61]:

local_ccy EUR USD

collateral_ccy usd usd

payment

2022-02-01 -20000000.00 20974233.02

2022-05-02 20000000.00 -20899604.66

An FXForward is a forward FX transaction.

In [62]: fxe = FXForward(

....: settlement=dt(2022, 4, 1),

....: pair="eurusd",

....: notional=10e6,

....: fx_rate=1.035,

....: )

....:

In [63]: fxe.rate(curves=[eurusd_curve, usd_curve], fx=fxf)

Out[63]: <Dual: 1.046264, (fx_eurusd), [1.0]>

In [64]: fxe.npv(curves=[eurusd_curve, usd_curve], fx=fxf)

Out[64]: <Dual: 106203.917957, (fx_eurusd), [9293922.1]>

In [65]: fxe.cashflows_table(curves=[eurusd_curve, usd_curve], fx=fxf)

Out[65]:

local_ccy EUR USD

collateral_ccy usd usd

payment

2022-04-01 10000000.00 -10350000.00

Cross-currency swaps (XCS) are easily configured and

analysed in rateslib.

In [66]: xcs = XCS(

....: effective=dt(2022, 4, 1),

....: termination="6m",

....: spec="eurusd_xcs",

....: float_spread=-3.0,

....: notional=25e6,

....: )

....:

In [67]: xcs.rate(curves=[eur_curve, eurusd_curve, usd_curve, usd_curve], fx=fxf)

Out[67]: <Dual: -10.421943, (fx_eurusd), [-0.0]>

In [68]: xcs.cashflows(curves=[eur_curve, eurusd_curve, usd_curve, usd_curve], fx=fxf)

Out[68]:

Type Ccy Payment Notional DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Period Convention DCF Acc Start Acc End Rate Spread FX Fixing FX Fix Date Reference Ccy

leg1 0 Cashflow EUR 2022-04-01 -25000000.00 0.99 25000000.00 24662055.24 1.00 EUR 24662055.24 usd NaN NaN NaN NaT NaT NaN NaN NaN NaT NaN

1 FloatPeriod EUR 2022-07-06 25000000.00 0.97 -357619.39 -348041.10 1.00 EUR -348041.10 usd Regular Act360 0.25 2022-04-01 2022-07-01 5.66 -3.00 NaN NaT NaN

2 FloatPeriod EUR 2022-10-05 25000000.00 0.98 106426.42 103996.26 1.00 EUR 103996.26 usd Regular Act360 0.26 2022-07-01 2022-10-03 -1.63 -3.00 NaN NaT NaN

3 Cashflow EUR 2022-10-03 25000000.00 0.98 -25000000.00 -24426969.29 1.00 EUR -24426969.29 usd NaN NaN NaN NaT NaT NaN NaN NaN NaT NaN

leg2 0 Cashflow USD 2022-04-01 25000000.00 0.99 -26156599.95 -25895158.01 1.00 USD -25895158.01 usd NaN NaN NaN NaT NaT NaN NaN 1.05 2022-03-30 EUR

1 FloatPeriod USD 2022-07-06 -25000000.00 0.98 267030.67 261469.06 1.00 USD 261469.06 usd Regular Act360 0.25 2022-04-01 2022-07-01 4.04 0.00 1.05 2022-03-30 EUR

2 MtmCashflow USD 2022-07-01 25000000.00 0.98 94099.95 92217.95 1.00 USD 92217.95 usd NaN NaN NaN NaT NaT NaN NaN 1.04 2022-06-29 EUR

3 FloatPeriod USD 2022-10-05 -25000000.00 0.96 417261.77 402336.93 1.00 USD 402336.93 usd Regular Act360 0.26 2022-07-01 2022-10-03 6.13 0.00 1.04 2022-06-29 EUR

4 Cashflow USD 2022-10-03 -25000000.00 0.96 26062500.00 25138777.08 1.00 USD 25138777.08 usd NaN NaN NaN NaT NaT NaN NaN 1.04 2022-06-29 EUR

In [69]: xcs.cashflows_table(curves=[eur_curve, eurusd_curve, usd_curve, usd_curve], fx=fxf)

Out[69]:

local_ccy EUR USD

collateral_ccy usd usd

payment

2022-04-01 25000000.00 -26156599.95

2022-07-01 0.00 94099.95

2022-07-06 -357619.39 267030.67

2022-10-03 -25000000.00 26062500.00

2022-10-05 106426.42 417261.77

Non-deliverable forwards (NDF) can be constructed.

In [70]: ndf = NDF(

....: settlement=dt(2022, 8, 15),

....: pair="eurusd",

....: notional=10e6, # 10mm EUR

....: fx_rate=1.1

....: )

....:

In [71]: ndf.rate(fx=fxf)

Out[71]: <Dual: 1.052563, (fx_eurusd), [1.0]>

In [72]: ndf.cashflows(curves=usd_curve, fx=fxf)

Out[72]:

Type Ccy Payment Notional DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral FX Fixing FX Fix Date Reference Ccy

leg1 0 Cashflow EUR 2022-08-15 -10000000.00 0.97 10000000.00 9725766.55 1.00 EUR 9725766.55 usd NaN NaT NaN

leg2 0 Cashflow EUR 2022-08-15 11000000.00 0.97 -10450682.94 -10164090.26 1.00 EUR -10164090.26 usd 1.05 2022-08-11 USD

In [73]: ndf.cashflows_table(curves=usd_curve, fx=fxf)

Out[73]:

local_ccy EUR

collateral_ccy usd

payment

2022-08-15 -450682.94

A Non-deliverable IRS (IRS) can be constructed.

In [74]: ndirs = IRS(

....: currency="usd", # <- local settlement currency

....: pair="eurusd", # <- EUR is the reference and notional currency

....: effective=dt(2022, 2, 1),

....: termination="2M",

....: frequency="M",

....: notional=10e6, # 10mm EUR

....: calendar="tgt|fed",

....: )

....:

In [75]: ndirs.rate(curves=[eur_curve, usd_curve], fx=fxf)

Out[75]: <Dual: 5.661639, (fx_eurusd), [0.0]>

In [76]: ndirs.cashflows(curves=[eur_curve, usd_curve], fx=fxf)

Out[76]:

Type Ccy Payment Notional Period Convention DCF Acc Start Acc End DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral Rate Spread FX Fixing FX Fix Date Reference Ccy

leg1 0 FixedPeriod USD 2022-03-03 10000000.00 Regular Act360 0.08 2022-02-01 2022-03-01 0.99 NaN NaN 1.00 USD NaN usd NaN NaN 1.05 2022-03-01 EUR

1 FixedPeriod USD 2022-04-05 10000000.00 Regular Act360 0.09 2022-03-01 2022-04-01 0.99 NaN NaN 1.00 USD NaN usd NaN NaN 1.05 2022-04-01 EUR

leg2 0 FloatPeriod USD 2022-03-03 -10000000.00 Regular Act360 0.08 2022-02-01 2022-03-01 0.99 46119.46 45806.51 1.00 USD 45806.51 usd 5.66 0.00 1.05 2022-03-01 EUR

1 FloatPeriod USD 2022-04-05 -10000000.00 Regular Act360 0.09 2022-03-01 2022-04-01 0.99 51006.15 50473.79 1.00 USD 50473.79 usd 5.66 0.00 1.05 2022-04-01 EUR

In [77]: ndirs.cashflows_table(curves=[eur_curve, usd_curve], fx=fxf)

Out[77]:

local_ccy USD

collateral_ccy usd

payment

2022-03-03 46119.46

2022-04-05 51006.15

A Non-deliverable XCS (NDXCS) can be constructed.

In [78]: ndxcs = NDXCS(

....: effective=dt(2022, 2, 1),

....: termination="2M",

....: currency="usd", # <- local settlement currency

....: pair="eurusd", # <- EUR is the reference and notional currency

....: frequency="M",

....: notional=10e6, # <- 10mm EUR set on Leg1

....: calendar="tgt|fed",

....: leg2_fx_fixings=1.2 # <- 12mm USD effectively set on Leg2

....: )

....:

In [79]: ndxcs.rate(curves=[eur_curve, usd_curve, usd_curve, usd_curve], fx=fxf)

Out[79]: <Dual: -20.450796, (fx_eurusd), [0.1]>

In [80]: ndxcs.cashflows(curves=[eur_curve, usd_curve, usd_curve, usd_curve], fx=fxf)

Out[80]:

Type Ccy Payment Notional DF Cashflow NPV FX Rate Base Ccy NPV Ccy Collateral FX Fixing FX Fix Date Reference Ccy Period Convention DCF Acc Start Acc End Rate Spread

leg1 0 Cashflow USD 2022-02-01 -10000000.00 1.00 10487116.51 10450892.41 1.00 USD 10450892.41 usd 1.05 2022-01-28 EUR NaN NaN NaN NaT NaT NaN NaN

1 FloatPeriod USD 2022-03-03 10000000.00 0.99 -46119.46 -45806.51 1.00 USD -45806.51 usd 1.05 2022-03-01 EUR Regular Act360 0.08 2022-02-01 2022-03-01 5.66 0.00

2 FloatPeriod USD 2022-04-05 10000000.00 0.99 -51006.15 -50473.79 1.00 USD -50473.79 usd 1.05 2022-04-01 EUR Regular Act360 0.09 2022-03-01 2022-04-01 5.66 0.00

3 Cashflow USD 2022-04-01 10000000.00 0.99 -10462639.98 -10358063.20 1.00 USD -10358063.20 usd 1.05 2022-03-30 EUR NaN NaN NaN NaT NaT NaN NaN

leg2 0 Cashflow USD 2022-02-01 10000000.00 1.00 -12000000.00 -11958550.17 1.00 USD -11958550.17 usd 1.20 2022-01-28 EUR NaN NaN NaN NaT NaT NaN NaN

1 FloatPeriod USD 2022-03-03 -10000000.00 0.99 37562.03 37307.16 1.00 USD 37307.16 usd 1.20 2022-01-28 EUR Regular Act360 0.08 2022-02-01 2022-03-01 4.02 0.00

2 FloatPeriod USD 2022-04-05 -10000000.00 0.99 41593.50 41159.39 1.00 USD 41159.39 usd 1.20 2022-01-28 EUR Regular Act360 0.09 2022-03-01 2022-04-01 4.03 0.00

3 Cashflow USD 2022-04-01 -10000000.00 0.99 12000000.00 11880056.91 1.00 USD 11880056.91 usd 1.20 2022-01-28 EUR NaN NaN NaN NaT NaT NaN NaN

In [81]: ndxcs.cashflows_table(curves=[eur_curve, usd_curve, usd_curve, usd_curve], fx=fxf)

Out[81]:

local_ccy USD

collateral_ccy usd

payment

2022-02-01 -1512883.49

2022-03-03 -8557.42

2022-04-01 1537360.02

2022-04-05 -9412.64

Calibrating curves with a solver#

The guide for Constructing Curves introduces the main

curve classes, Curve and LineCurve.

It also touches on some of the more

advanced curves CompositeCurve,

ProxyCurve, and MultiCsaCurve.

Calibrating curves is a very natural thing to do in fixed income. We typically use market prices of commonly traded instruments to set values. Smiles and Surfaces are also calibrated using the same optimising algorithms.

Below we demonstrate how to calibrate the Curve that

we created above in the initial trivial example using SOFR swap market data.

In this case we invoke the Solver which forces mutations to the

provided curves making sure they reprice the provided calibrating instruments at the

gives rates s.

In this case we target the 6M and 1Y IRS rates.

In [82]: solver = Solver(

....: curves=[usd_curve],

....: instruments=[

....: IRS(dt(2022, 1, 1), "6M", spec="usd_irs", curves="sofr"),

....: IRS(dt(2022, 1, 1), "1Y", spec="usd_irs", curves="sofr"),

....: ],

....: s=[4.35, 4.85],

....: instrument_labels=["6M", "1Y"],

....: id="us_rates"

....: )

....:

SUCCESS: `func_tol` reached after 3 iterations (levenberg_marquardt), `f_val`: 3.0486414271327023e-15, `time`: 0.0012s

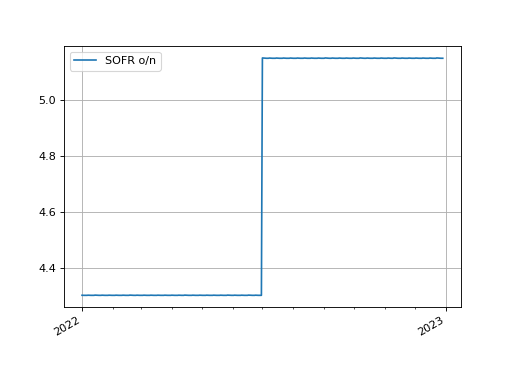

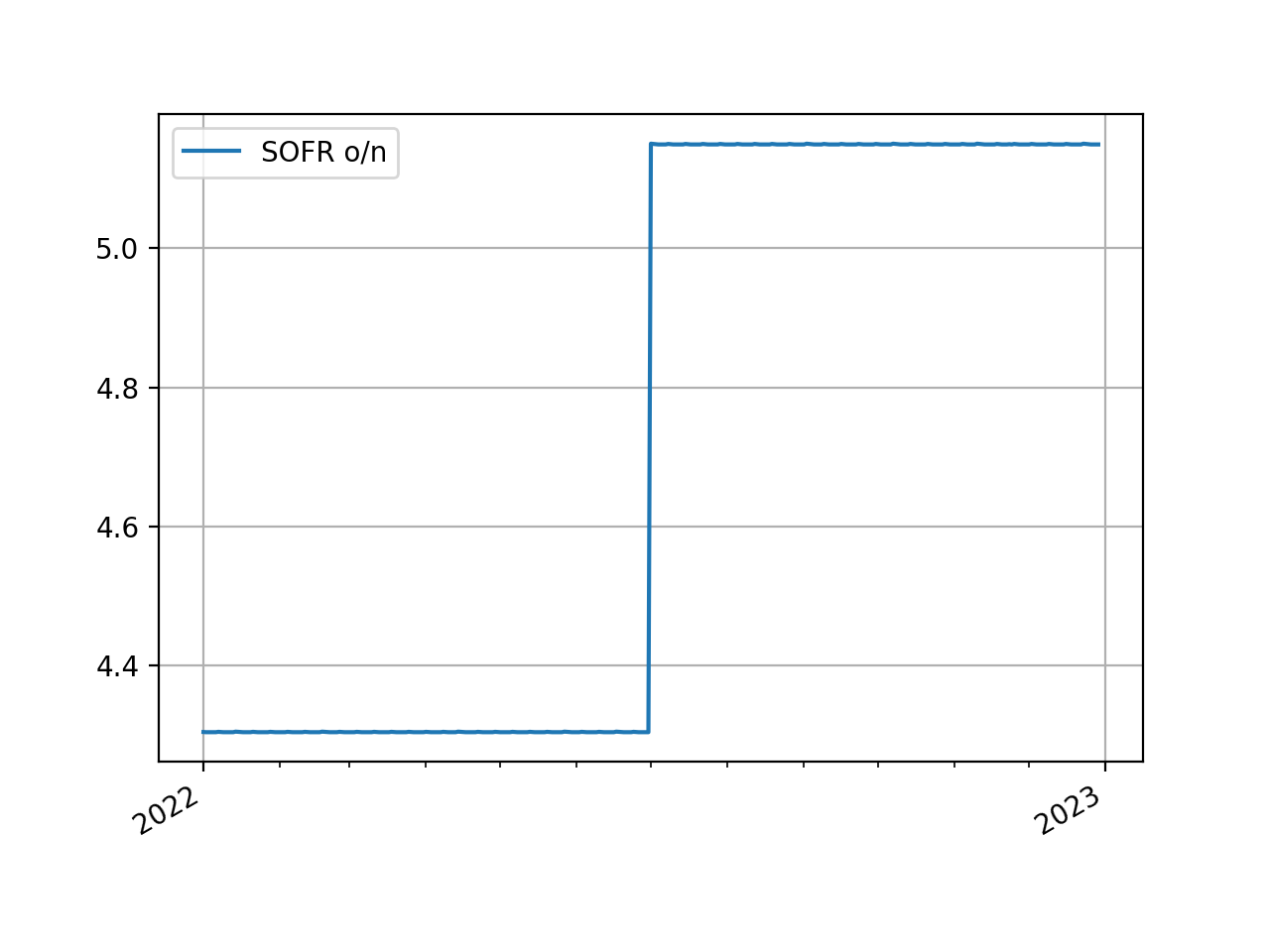

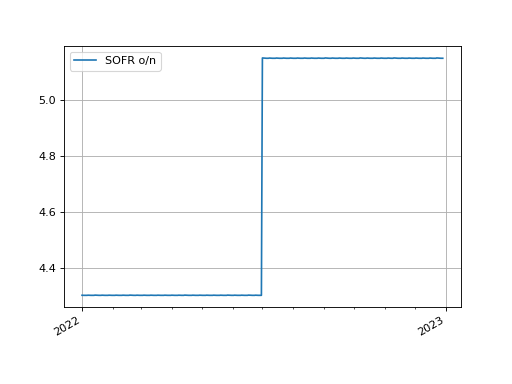

Solving was a success! Observe that the DFs on the Curve have been updated:

In [83]: usd_curve.nodes

Out[83]: _CurveNodes(_nodes={datetime.datetime(2022, 1, 1, 0, 0): <Dual: 1.000000, (sofr0, sofr1, sofr2), [1.0, 0.0, 0.0]>, datetime.datetime(2022, 7, 1, 0, 0): <Dual: 0.978595, (sofr0, sofr1, sofr2), [0.0, 1.0, 0.0]>, datetime.datetime(2023, 1, 1, 0, 0): <Dual: 0.953176, (sofr0, sofr1, sofr2), [0.0, 0.0, 1.0]>})

We can plot the overnight rates for the calibrated curve. This curve uses ‘log_linear’ interpolation so the overnight forward rates are constant between node dates.

In [84]: usd_curve.plot("1b", labels=["SOFR o/n"])

Out[84]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x170b71a90>])

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

Risk Sensitivities#

Rateslib’s can calculate delta and cross-gamma risks relative to the calibrating Instruments of a Solver. Rateslib also unifies these risks against the FX rates used to create an FXForwards market, to provide a fully consistent risk framework expressed in arbitrary currencies. See the risk framework notes.

Performance wise, because rateslib uses dual number AD upto 2nd order, combined with the appropriate analysis, it is shown to calculate a 150x150 Instrument cross-gamma grid (22,500 elements) from a calculated portfolio NPV in approximately 250ms.

Scheduling#

Necessary functionality is provided natively by rateslib. See:

Utilities#

Rateslib could not function without some utility libraries. These are often referenced in other guides as they arise and can also be linked to from those sections.

Specifically those utilities are:

Cookbook#

This is a collection of more detailed examples and explanations that don’t necessarily fall into any one category. See the Cookbook index.

Advanced Concepts#

These sections describe and exemplify some of the architectural choices in rateslib.

Pricing Mechanisms#

Since rateslib is an object oriented library with object associations we give detailed instructions of the way in which the associations can be constructed in mechanisms.

The key takeway is that when you initialise and create an Instrument you can do one of three things:

Not provide any Curves (or Vol surface) for pricing upfront (

curves=NoInput(0)).Create an explicit association to pre-existing Python objects, e.g.

curves=my_curve.Define some reference to a Curves mapping with strings using

curves="my_curve_id".

If you do 1) then you must provide Curves at price

time: instrument.npv(curves=my_curve).

If you do 2) then you do not need to provide anything further at price time:

instrument.npv(). But you still can provide Curves directly, like for 1), as an override.

If you do 3) then you can provide a Solver which contains the Curves and will

resolve the string mapping: instrument.npv(solver=my_solver). But you can also provide Curves

directly, like for 1), as an override.

Best practice in rateslib is to use 3). This is the safest and most flexible approach and designed to work best with risk sensitivity calculations also.

Mutability#

A proper outline of the mutability of objects is given in mutability.

In summary, best practice is to create new instances and avoid directly overwriting or adding

to class attributes. Don’t mutate a created object unless using an official method to do so,

e.g. FXRates.update or

Curve.update