Inflation Indexes and Curves 2 (Quantlib comparison)#

This guide replicates and is a comparison to the Quantlib tutorial page at https://www.quantlibguide.com/Inflation%20indexes%20and%20curves.html

Inflation Indexes#

Historical index fixings in rateslib should be indexed to the 1st of the appropriate inflation month.

[1]:

from rateslib import *

from pandas import Series, MultiIndex

[2]:

inflation_fixings = [

(dt(2022, 1, 1), 110.70),

(dt(2022, 2, 1), 111.74),

(dt(2022, 3, 1), 114.46),

(dt(2022, 4, 1), 115.11),

(dt(2022, 5, 1), 116.07),

(dt(2022, 6, 1), 117.01),

(dt(2022, 7, 1), 117.14),

(dt(2022, 8, 1), 117.85),

(dt(2022, 9, 1), 119.26),

(dt(2022, 10, 1), 121.03),

(dt(2022, 11, 1), 120.95),

(dt(2022, 12, 1), 120.52),

(dt(2023, 1, 1), 120.27),

(dt(2023, 2, 1), 121.24),

(dt(2023, 3, 1), 122.34),

(dt(2023, 4, 1), 123.12),

(dt(2023, 5, 1), 123.15),

(dt(2023, 6, 1), 123.47),

(dt(2023, 7, 1), 123.36),

(dt(2023, 8, 1), 124.03),

(dt(2023, 9, 1), 124.43),

(dt(2023, 10, 1), 124.54),

(dt(2023, 11, 1), 123.85),

(dt(2023, 12, 1), 124.05),

(dt(2024, 1, 1), 123.60),

(dt(2024, 2, 1), 124.37),

(dt(2024, 3, 1), 125.31),

(dt(2024, 4, 1), 126.05),

]

dates, values = zip(*inflation_fixings)

fixings.add("cpi_fixings", Series(values, dates))

Rateslib contains an index_value method that will determine such for a given reference value date and other common parameters.

[3]:

index_value(

index_lag=0,

index_method="monthly",

index_fixings="cpi_fixings",

index_date=dt(2024, 3, 15)

)

[3]:

np.float64(125.31)

For example to replicate the Quantlib example of a lagged reference date we can use:

[4]:

index_value(

index_lag=3,

index_method="daily",

index_fixings="cpi_fixings",

index_date=dt(2024, 5, 15)

)

[4]:

np.float64(124.79451612903226)

Inflation Curves#

Create a nominal discount curve for cashflows. Calibrated to a 3% continuously compounded rate.

[5]:

nominal_curve = Curve(

nodes={dt(2024, 5, 11): 1.0, dt(2074, 5, 18): 1.0},

interpolation="log_linear",

convention="Act365F",

id="discount"

)

solver1 = Solver(

curves=[nominal_curve],

instruments=[Value(dt(2074, 5, 11), metric="cc_zero_rate", curves="discount")],

s=[3.0],

id="rates",

instrument_labels=["nominal"],

)

SUCCESS: `func_tol` reached after 7 iterations (levenberg_marquardt), `f_val`: 7.1651768419373015e-12, `time`: 0.0011s

Now create an inflation curve, based on the last known CPI print, calibrated with zero coupon inflation swaps rates. Notice that an inflation curve starts as of the last known fixing as its index_base. This is similar to Quantlib, not be design, but by necessity since this is the only information we have that can define the start of the curve.

[6]:

inflation_curve = Curve(

nodes={

dt(2024, 4, 1): 1.0, # <- last known inflation print.

dt(2025, 5, 11): 1.0, # 1y

dt(2026, 5, 11): 1.0, # 2y

dt(2027, 5, 11): 1.0, # 3y

dt(2028, 5, 11): 1.0, # 4y

dt(2029, 5, 11): 1.0, # 5y

dt(2031, 5, 11): 1.0, # 7y

dt(2034, 5, 11): 1.0, # 10y

dt(2036, 5, 11): 1.0, # 12y

dt(2039, 5, 11): 1.0, # 15y

dt(2044, 5, 11): 1.0, # 20y

dt(2049, 5, 11): 1.0, # 25y

dt(2054, 5, 11): 1.0, # 30y

dt(2064, 5, 11): 1.0, # 40y

dt(2074, 5, 11): 1.0, # 50y

},

interpolation="log_linear",

convention="Act365F",

index_base=126.05,

index_lag=0,

id="inflation"

)

solver = Solver(

pre_solvers=[solver1],

curves=[inflation_curve],

instruments=[

ZCIS(dt(2024, 5, 11), "1y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "2y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "3y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "4y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "5y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "7y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "10y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "12y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "15y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "20y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "25y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "30y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "40y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "50y", spec="eur_zcis", curves=["inflation", "discount"], leg2_index_fixings="cpi_fixings"),

],

s=[2.93, 2.95, 2.965, 2.98, 3.0, 3.06, 3.175, 3.243, 3.293, 3.338, 3.348, 3.348, 3.308, 3.228],

instrument_labels=["1y", "2y", "3y", "4y", "5y", "7y", "10y", "12y", "15", "20y", "25y", "30y", "40y", "50y"],

id="zcis",

)

SUCCESS: `func_tol` reached after 8 iterations (levenberg_marquardt), `f_val`: 1.4302416694642844e-17, `time`: 0.0153s

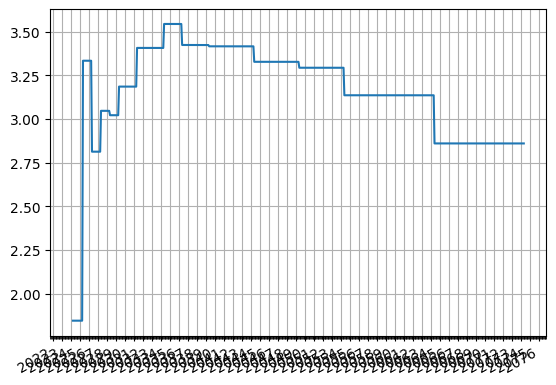

The data can be output to a table or plotted as below.

[7]:

inflation_curve.plot("1m")

[7]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x116a416a0>])

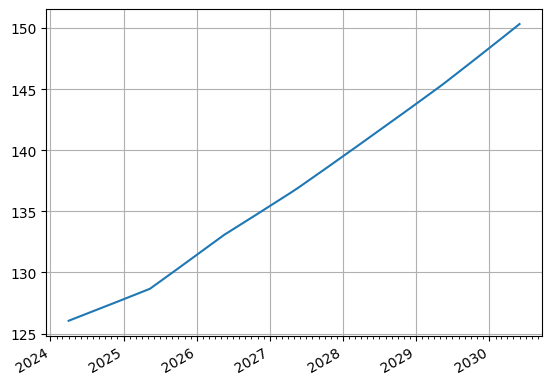

[8]:

inflation_curve.plot_index(right=dt(2030, 6, 1))

[8]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x1176e7620>])

Some of the forecast values from the curve can be obtained directly from Curve methods.

[9]:

inflation_curve.index_value(dt(2027, 4, 1), index_lag=3, index_method="monthly")

[9]:

<Dual: 135.440324, (inflation0, inflation1, inflation2, ...), [-0.0, -0.0, -50.9, ...]>

[10]:

inflation_curve.index_value(dt(2027, 4, 1), index_lag=0, index_method="monthly")

[10]:

<Dual: 136.382058, (inflation0, inflation1, inflation2, ...), [-0.0, -0.0, -15.8, ...]>

[11]:

inflation_curve.index_value(dt(2027, 5, 15), index_lag=3, index_method="daily")

[11]:

<Dual: 135.896278, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, -33.9, ...]>

Seasonality#

The way rateslib handles seasonality is to replicate it via its CompositeCurve framework. With this approach, adding seasonality can be done in a multitude of ways, but since Quantlib has used seasonaility factors we will synthesize that approach within rateslib’s framework. We create a new curve with node dates reflecting the key dates used by Quantlib.

The theory here for rateslib is as follows.

A discount factor on a rateslib CompositeCurve is very approximately the product of the discount factors of its contained curves (c1 and c2):

The CompositeCurve index value takes its index base from the first (main) curve in its composition, therefore the index value is calculated according to:

If we set the index base on the seasonality curve (c2) exactly to 1.0 this equation reduces to:

So the index value on the CompositeCurve equals the product of the two index values.

Thus, if we set the set the index values on the seasonality curve (c2) directly they can act directly as multipliers to the underlying inflation values on the inflation curve. This seasonality curve can be calibrated using a Solver, and in this particular case (to match Quantlib) they are calibrated directly with index values.

Here we add the same seasonality factors in years 2025, 2026 and 2027.

[12]:

season = Curve(

nodes={

dt(2024, 4, 1): 1.0,

dt(2024, 12, 1): 1.0,

**{dt(2025, _, 1): 1.0 for _ in range(1, 13)},

**{dt(2026, _, 1): 1.0 for _ in range(1, 13)},

**{dt(2027, _, 1): 1.0 for _ in range(1, 13)},

dt(2074, 5, 11): 1.0,

},

interpolation="log_linear",

convention="Act365F",

index_base=1.0, # <- as per theory above

index_lag=0, # <- matches the main inflation curve

id="seasonality"

)

The seasonality factors will be added by directly inserting index values at specific dates.

[13]:

yearly_multipliers = [

1.003245,

1.001994,

0.999715,

1.000495,

1.000929,

0.998687,

0.995949,

0.994682,

0.995949,

1.000519,

1.003705,

1.004186,

]

season_solver = Solver(

curves=[season],

instruments=\

[Value(dt(2024, 12, 1), curves=[season], metric="index_value")] +\

[Value(dt(2025, _, 1), curves=[season], metric="index_value") for _ in range(1, 13)] +\

[Value(dt(2026, _, 1), curves=[season], metric="index_value") for _ in range(1, 13)] +\

[Value(dt(2027, _, 1), curves=[season], metric="index_value") for _ in range(1, 13)],

s=[1.0] + yearly_multipliers*3

)

SUCCESS: `func_tol` reached after 8 iterations (levenberg_marquardt), `f_val`: 1.290941550558499e-12, `time`: 0.0206s

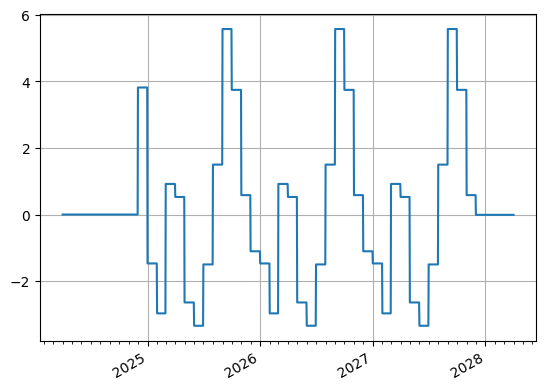

[14]:

season.plot("1b", left=dt(2024, 4, 1), right=dt(2028, 4, 1))

[14]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x11785e510>])

Once the seasonality is designed it must be composited with an underlying inflation curve and the instruments re-solved

[15]:

inflation_with_season = CompositeCurve([inflation_curve, season], id="inflation_s")

[16]:

solver = Solver(

pre_solvers=[solver1], # nominal discount curve

curves=[inflation_with_season, inflation_curve],

instruments=[

ZCIS(dt(2024, 5, 11), "1y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "2y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "3y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "4y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "5y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "7y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "10y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "12y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "15y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "20y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "25y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "30y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "40y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

ZCIS(dt(2024, 5, 11), "50y", spec="eur_zcis", curves=["inflation_s", "discount"], leg2_index_fixings="cpi_fixings"),

],

s=[2.93, 2.95, 2.965, 2.98, 3.0, 3.06, 3.175, 3.243, 3.293, 3.338, 3.348, 3.348, 3.308, 3.228],

instrument_labels=["1y", "2y", "3y", "4y", "5y", "7y", "10y", "12y", "15y", "20y", "25y", "30y", "40y", "50y"],

id="zcis",

)

SUCCESS: `func_tol` reached after 5 iterations (levenberg_marquardt), `f_val`: 1.7223655493350175e-13, `time`: 0.0145s

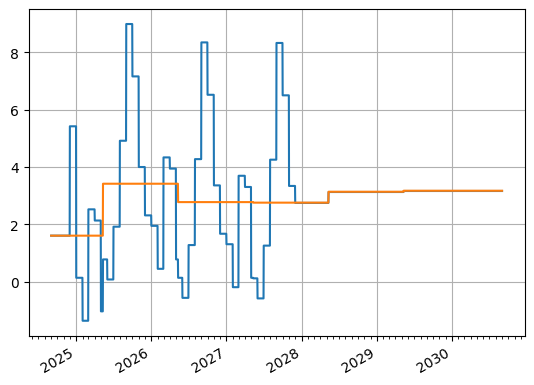

[17]:

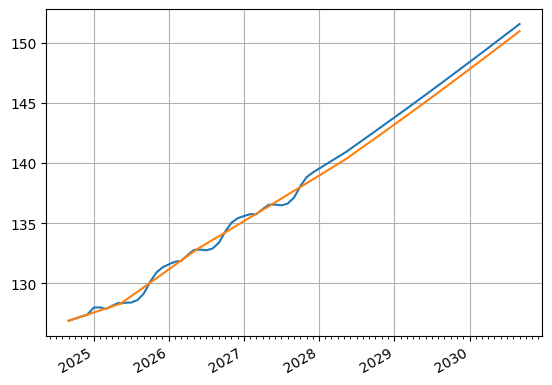

inflation_with_season.plot("1b", comparators=[inflation_curve], left=dt(2024, 9, 1), right=dt(2030, 9, 1))

[17]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x117b1eba0>,

<matplotlib.lines.Line2D at 0x117b1ecf0>])

[18]:

inflation_with_season.plot_index(comparators=[inflation_curve], left=dt(2024, 9, 1), right=dt(2030, 9, 1))

[18]:

(<Figure size 640x480 with 1 Axes>,

<Axes: >,

[<matplotlib.lines.Line2D at 0x120994ec0>,

<matplotlib.lines.Line2D at 0x120995010>])

New sampled values#

[19]:

inflation_with_season.index_value(dt(2027, 4, 1), index_lag=3, index_method="monthly")

[19]:

<Dual: 135.613192, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, -50.9, ...]>

[20]:

inflation_with_season.index_value(dt(2027, 4, 1), index_lag=0, index_method="monthly")

[20]:

<Dual: 136.170810, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, -15.7, ...]>

[21]:

inflation_with_season.index_value(dt(2027, 5, 15), index_lag=3, index_method="daily")

[21]:

<Dual: 135.754993, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, -33.8, ...]>

The trick here is obviously to find a representation of a seasonality curve that matches one’s expectation of seasonality adjustments. Here, a Solver calibration was used to separately solve the seasonality curve to inflation rate adjustments.

[22]:

for i, date in enumerate([dt(2025, _, 1) for _ in range(1, 13)]+[dt(2026, _, 1) for _ in range(1, 13)]):

a = inflation_curve.index_value(date, index_lag=0, index_method="monthly")

b = inflation_with_season.index_value(date, index_lag=0, index_method="monthly")

print(f"Date: {date}, Inflation curve: {float(a):.5f}, With seasonality: {float(b):.5f}, Multiplier: {float(b/a):.7f}, Intended Multiplier: {yearly_multipliers[i%12]:.7f}")

Date: 2025-01-01 00:00:00, Inflation curve: 127.58510, With seasonality: 127.99907, Multiplier: 1.0032447, Intended Multiplier: 1.0032450

Date: 2025-02-01 00:00:00, Inflation curve: 127.75932, With seasonality: 128.01404, Multiplier: 1.0019938, Intended Multiplier: 1.0019940

Date: 2025-03-01 00:00:00, Inflation curve: 127.91688, With seasonality: 127.88042, Multiplier: 0.9997150, Intended Multiplier: 0.9997150

Date: 2025-04-01 00:00:00, Inflation curve: 128.09155, With seasonality: 128.15494, Multiplier: 1.0004949, Intended Multiplier: 1.0004950

Date: 2025-05-01 00:00:00, Inflation curve: 128.26081, With seasonality: 128.37995, Multiplier: 1.0009289, Intended Multiplier: 1.0009290

Date: 2025-06-01 00:00:00, Inflation curve: 128.56987, With seasonality: 128.40108, Multiplier: 0.9986871, Intended Multiplier: 0.9986870

Date: 2025-07-01 00:00:00, Inflation curve: 128.93158, With seasonality: 128.40934, Multiplier: 0.9959495, Intended Multiplier: 0.9959490

Date: 2025-08-01 00:00:00, Inflation curve: 129.30641, With seasonality: 128.61884, Multiplier: 0.9946826, Intended Multiplier: 0.9946820

Date: 2025-09-01 00:00:00, Inflation curve: 129.68234, With seasonality: 129.15706, Multiplier: 0.9959495, Intended Multiplier: 0.9959490

Date: 2025-10-01 00:00:00, Inflation curve: 130.04718, With seasonality: 130.11466, Multiplier: 1.0005189, Intended Multiplier: 1.0005190

Date: 2025-11-01 00:00:00, Inflation curve: 130.42525, With seasonality: 130.90842, Multiplier: 1.0037046, Intended Multiplier: 1.0037050

Date: 2025-12-01 00:00:00, Inflation curve: 130.79218, With seasonality: 131.33961, Multiplier: 1.0041855, Intended Multiplier: 1.0041860

Date: 2026-01-01 00:00:00, Inflation curve: 131.17243, With seasonality: 131.59803, Multiplier: 1.0032446, Intended Multiplier: 1.0032450

Date: 2026-02-01 00:00:00, Inflation curve: 131.55378, With seasonality: 131.81606, Multiplier: 1.0019938, Intended Multiplier: 1.0019940

Date: 2026-03-01 00:00:00, Inflation curve: 131.89917, With seasonality: 131.86159, Multiplier: 0.9997150, Intended Multiplier: 0.9997150

Date: 2026-04-01 00:00:00, Inflation curve: 132.28264, With seasonality: 132.34811, Multiplier: 1.0004949, Intended Multiplier: 1.0004950

Date: 2026-05-01 00:00:00, Inflation curve: 132.65479, With seasonality: 132.77801, Multiplier: 1.0009289, Intended Multiplier: 1.0009290

Date: 2026-06-01 00:00:00, Inflation curve: 132.99141, With seasonality: 132.81681, Multiplier: 0.9986872, Intended Multiplier: 0.9986870

Date: 2026-07-01 00:00:00, Inflation curve: 133.29532, With seasonality: 132.75542, Multiplier: 0.9959495, Intended Multiplier: 0.9959490

Date: 2026-08-01 00:00:00, Inflation curve: 133.61010, With seasonality: 132.89966, Multiplier: 0.9946827, Intended Multiplier: 0.9946820

Date: 2026-09-01 00:00:00, Inflation curve: 133.92562, With seasonality: 133.38316, Multiplier: 0.9959495, Intended Multiplier: 0.9959490

Date: 2026-10-01 00:00:00, Inflation curve: 134.23168, With seasonality: 134.30133, Multiplier: 1.0005189, Intended Multiplier: 1.0005190

Date: 2026-11-01 00:00:00, Inflation curve: 134.54867, With seasonality: 135.04711, Multiplier: 1.0037045, Intended Multiplier: 1.0037050

Date: 2026-12-01 00:00:00, Inflation curve: 134.85614, With seasonality: 135.42058, Multiplier: 1.0041855, Intended Multiplier: 1.0041860

Inflation Swap and DV01#

We can easily construct a ZCIS or other type of inflation based instrument and use the native delta and gamma methods associated with a Solver to extract risk sensitivities.

[23]:

zcis = ZCIS(dt(2024, 3, 11), "4y", spec="eur_zcis", curves=["inflation_s", "discount"], fixed_rate=3.0, leg2_index_fixings="cpi_fixings")

[24]:

zcis.rate(solver=solver)

[24]:

<Dual: 2.926124, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, 0.0, ...]>

[25]:

zcis.npv(solver=solver)

[25]:

<Dual: -2874.505227, (inflation0, inflation1, inflation2, ...), [0.0, 0.0, 0.0, ...]>

[26]:

df = zcis.delta(solver=solver)

descriptors = df.agg(["sum"])

descriptors.index = MultiIndex.from_tuples([("sum", "sum", "sum")])

df.style.format(precision=0).concat(descriptors.style.format(precision=0))

[26]:

| local_ccy | eur | ||

|---|---|---|---|

| display_ccy | eur | ||

| type | solver | label | |

| instruments | rates | nominal | 1 |

| zcis | 1y | 4 | |

| 2y | -23 | ||

| 3y | 93 | ||

| 4y | 298 | ||

| 5y | -0 | ||

| 7y | -0 | ||

| 10y | 0 | ||

| 12y | 0 | ||

| 15y | 0 | ||

| 20y | 0 | ||

| 25y | -0 | ||

| 30y | 0 | ||

| 40y | -0 | ||

| 50y | -0 | ||

| sum | sum | sum | 373 |

This risk display shows no exposure to the seasonality configuration becuase the Solver that was used to calibrate the seasonality was not added as a pre_solver to the Solver used in the last step. Therefore it treats the seasonality as a constant and not as variable to which risk sensitivities can be obtained.

To observe the change, simply replace pre_solvers=[solver1] with pre_solvers=[solver1, season_solver], in the above Solver and re run the cells.

[27]:

zcis.gamma(solver=solver).style.format(precision=1)

[27]:

| type | instruments | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| solver | rates | zcis | |||||||||||||||||

| label | nominal | 1y | 2y | 3y | 4y | 5y | 7y | 10y | 12y | 15y | 20y | 25y | 30y | 40y | 50y | ||||

| local_ccy | display_ccy | type | solver | label | |||||||||||||||

| eur | eur | instruments | rates | nominal | -0.0 | -0.0 | 0.0 | -0.0 | -0.1 | 0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 |

| zcis | 1y | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | -0.0 | |||

| 2y | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | ||||

| 3y | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | -0.0 | ||||

| 4y | -0.1 | 0.0 | -0.0 | 0.0 | 0.1 | -0.0 | -0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.0 | -0.0 | ||||

| 5y | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 7y | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 10y | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 12y | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 15y | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 20y | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 25y | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | -0.0 | ||||

| 30y | -0.0 | 0.0 | -0.0 | 0.0 | 0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | ||||

| 40y | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | ||||

| 50y | 0.0 | -0.0 | 0.0 | -0.0 | -0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | -0.0 | 0.0 | ||||

[ ]: